Imagine a letter arrives one morning with the Revenue Commissioners logo in the top corner. You’re not in trouble yet — it’s a notification that your business has been selected for a compliance check. You have a few weeks to get your records together.

Now ask yourself: could you put your hands on six years of sequentially numbered invoices, purchase records, cash logs, and stock reconciliations within a reasonable timeframe? Would your records hold up to scrutiny, or would you spend the intervening weeks hoping the inspector doesn’t look too closely at 2023?

This is the reality of Revenue compliance for garages. It doesn’t happen to every business every year — but it does happen, and when it does, the state of your records is what determines whether it’s a straightforward process or a stressful and expensive one.

This guide covers what Revenue looks for when they examine an Irish garage, the record-keeping requirements you need to meet, and how running the business through proper management software creates an audit trail that essentially manages compliance for you.

Why garages attract Revenue attention

Revenue doesn’t select businesses for compliance checks at random. Certain industries and certain patterns draw attention, and garages tend to tick several boxes.

High cash turnover. Garages — particularly smaller independent workshops — still handle significant cash. Cash-intensive businesses are a well-known area of focus for Revenue because cash is harder to trace than card transactions. If your declared income doesn’t match what would reasonably be expected for a business of your size and type, that gap is something Revenue will want to understand.

Mixed VAT rates. Garage work spans multiple VAT rates — 23% on standalone parts, 13.5% on labour and repair services. Businesses that apply mixed rates have more opportunity for error (deliberate or otherwise) and receive more scrutiny as a result. Revenue has seen enough garages apply a single rate across all lines to know it’s a common problem.

High parts spend relative to revenue. If the parts you’re claiming as business expenses don’t match the repair work you’re invoicing, that discrepancy raises questions about stock, cash jobs, or record accuracy.

Sector intelligence. Revenue conducts compliance campaigns by sector. If they’ve identified a pattern of under-reporting across the motor trade nationally, garages broadly become a focus — not just the ones with obvious red flags.

None of this means you’re doing anything wrong. It means garages operate in an environment where Revenue pays attention, and your records need to reflect that.

What Revenue actually looks for in a garage audit

A Revenue compliance check for a garage will typically examine several areas.

Income completeness

Revenue will compare your declared income against external indicators — bank lodgements, card terminal records, supplier invoices, and where possible, data from third parties like parts suppliers or insurance companies. If your invoiced revenue is significantly lower than what these indicators suggest it should be, you’ll need to explain the difference.

This is where cash handling discipline becomes critical. Every transaction — card or cash — needs to end up on an invoice and in your records. A pattern of cash payments that don’t appear to flow through to declared income is exactly what a compliance check is designed to find.

VAT accuracy

Revenue will check that VAT has been correctly charged, correctly calculated, and correctly declared on your VAT returns. For a garage, this means verifying that the right rate has been applied to each type of supply — 13.5% for labour and repair services, 23% for standalone parts and accessories — and that the amounts declared on your returns match your invoices.

They will also check that VAT on your purchase invoices (the input tax you’re claiming back) corresponds to genuine business purchases supported by valid supplier invoices.

Payroll and PAYE

If you employ technicians or other staff, Revenue will check that PAYE and PRSI are being operated correctly through Revenue’s Online Service (ROS). Underpaying or misclassifying workers — treating employees as contractors to avoid employer obligations, for example — is an area of active enforcement.

Stock and parts reconciliation

One of the more detailed checks in a garage audit is comparing parts purchased against parts invoiced to customers. If you bought significantly more in parts than appears on customer invoices, Revenue will want to understand where the difference went — warranty use, waste, or work that was done but not invoiced.

Proper stock reconciliation, where what you ordered is matched against what you used on each job, is what closes this gap.

Cash handling procedures

If your garage takes cash, Revenue will examine how it’s handled. They’ll look for evidence of a consistent process: cash received is issued with an invoice or receipt, cash receipts are recorded in a cash register or equivalent system, daily cash is reconciled against invoiced amounts, and lodgements match what was taken in.

A business that takes cash but has no coherent system for recording and reconciling it — no Z-reads from a till, no cash book, just a rough sense of what came in — is vulnerable. Even if every cent has been declared correctly, the absence of a documented process makes it very difficult to demonstrate that.

Record-keeping requirements for Irish garages

Revenue’s requirements for business record-keeping are set out under the Taxes Consolidation Act 1997. The rules are not ambiguous, and they apply whether you’re a sole trader or a limited company.

What records you must keep

You are required to keep full and accurate records sufficient to allow your tax returns to be verified. For a garage, this includes:

- Sales records. Every invoice issued, in sequential order, with no gaps. For cash sales, a receipt or invoice must be issued and retained.

- Purchase records. All supplier invoices, receipts, and delivery dockets for parts and materials bought for the business.

- Bank records. Bank statements, lodgement books, and any supporting documentation for business transactions.

- Payroll records. Records of wages, PAYE and PRSI paid, and employment details for each employee.

- VAT records. A record of all taxable supplies and purchases, sufficient to support each VAT return filed.

- Cash records. Till rolls or equivalent documentation showing daily cash taken in, and records reconciling cash receipts to lodgements.

The standard Revenue sets is that your records must be sufficient for an authorised officer to verify that your tax returns are correct. That’s a practical test: if an inspector sat down with your records, could they trace a transaction from customer payment through to your bank account and your tax return?

The six-year retention rule

All business records must be retained for a minimum of six years from the end of the accounting period to which they relate. This is the rule most garage owners underestimate.

It doesn’t mean six years from today. It means six years from the end of the year the records relate to. Records from the 2020 tax year need to be kept until at least the end of 2026. If Revenue opens an enquiry into your 2021 returns in 2025, you need 2021 records available in full.

In practical terms, this means whatever system you use to store invoices, purchase records, and financial documents must be able to retrieve records going back six years. A folder of PDFs on a laptop that gets replaced every three years is not a reliable six-year archive. A cloud-based system that stores everything centrally and maintains it regardless of what happens to any individual device is.

Cash handling: the area most garages get wrong

Cash is where Revenue compliance problems most often originate for garages — not necessarily because money is being hidden, but because cash handling processes are inconsistent or undocumented.

The standard you need to meet is straightforward: every cash transaction must generate a record at the point of sale, and that record must be reconcilable with your bank lodgements.

In practice, this means:

Issue a receipt or invoice for every cash transaction. Not sometimes, not for amounts over a certain threshold — every time. If a customer pays €80 cash for a tyre change, there needs to be a record of that €80.

Record daily cash takings separately. A cash book, a till report (Z-read), or an equivalent daily cash reconciliation shows what came in during the day, what was in the till at the start, and what was lodged. This is what makes cash traceable.

Lodge cash consistently. Irregular lodgement patterns — some weeks you lodge daily, other weeks money sits in a drawer — make reconciliation difficult and create questions about what happened between the transaction and the bank.

Don’t use cash takings to pay expenses directly. Paying a supplier or a casual worker from the day’s cash, without recording the transaction, removes money from your records in a way that’s difficult to reconstruct later. Every expense should go through a proper payment process with documentation.

None of these are difficult requirements. What makes cash compliance challenging is consistency — applying the same process every day, not just when you remember. A system where cash sales are entered into the same software that handles your invoicing and card transactions makes that consistency much easier to maintain.

Stock reconciliation: matching parts to jobs

Parts reconciliation is a Revenue requirement that many garages handle poorly — not because they’re doing anything improper, but because their systems don’t make it easy to track parts from purchase through to use.

The basic discipline is: every part you purchase for the business should eventually appear on a customer invoice or be accounted for in another way (warranty use, write-off, returned to supplier). If parts are disappearing from your records without appearing on invoices, that’s a discrepancy that needs explaining.

In a well-run system, this works as follows:

- Parts are ordered through a purchase order linked to a specific job.

- When parts arrive, they’re received against the purchase order.

- Parts are added to the job card and appear on the customer invoice when the job is completed.

- At any point, you can see what parts are on hand, what’s been ordered, and what’s been invoiced — and the numbers should reconcile.

When a garage orders parts informally — by phone, paid on account, entered manually later — the link between purchase and use breaks down. Parts arrive, get used, and may or may not make it onto the job card, depending on whether someone remembered. This is how stock discrepancies develop, and it’s exactly what a Revenue audit is designed to identify.

Purchase orders linked to jobs solve this at the process level. Every part ordered for a job is recorded at the time of ordering, received against that order, and flows through to the customer invoice automatically. The reconciliation happens as part of the normal workflow, rather than as a separate exercise at month-end or audit time.

VAT compliance: the specifics for garages

VAT compliance deserves its own section because garage businesses have more complexity here than most service businesses.

The rates that apply are:

- 13.5% for repair, maintenance, and servicing of motor vehicles — this covers labour and parts supplied as part of a repair or service (the composite supply rule applies where parts are integral to the service).

- 23% for parts and accessories supplied separately — parts sold at retail, accessories, tyres supplied independently of a service.

A typical garage invoice can include both rates. An oil service might include labour and included parts at 13.5%, and an air freshener or wiper blades sold separately at 23%. Both need to be shown separately on the invoice with the correct rate applied to each.

The errors Revenue finds most often in garages are applying a single rate across all lines, applying the wrong rate to tyre-only sales (which should be 23% when sold separately), and failing to declare the correct VAT amounts on periodic returns.

Your VAT returns, filed through ROS, must match what’s on your invoices. Revenue has the ability to cross-reference declared VAT against invoice data, and significant discrepancies are flagged automatically.

For a more detailed look at how VAT works in the context of garage billing, including the composite supply rules and how to handle mixed-rate invoices, the VAT for garages guide covers this in full.

How software creates an audit trail automatically

The reason Revenue compliance is stressful for many garage owners is that it requires information that’s spread across different places — invoices in one system, purchase records in another, cash in a till roll from three years ago that may or may not still exist.

When your garage runs through a single integrated system, compliance is largely a by-product of normal operations rather than something you have to manage separately.

Here is what that looks like in practice.

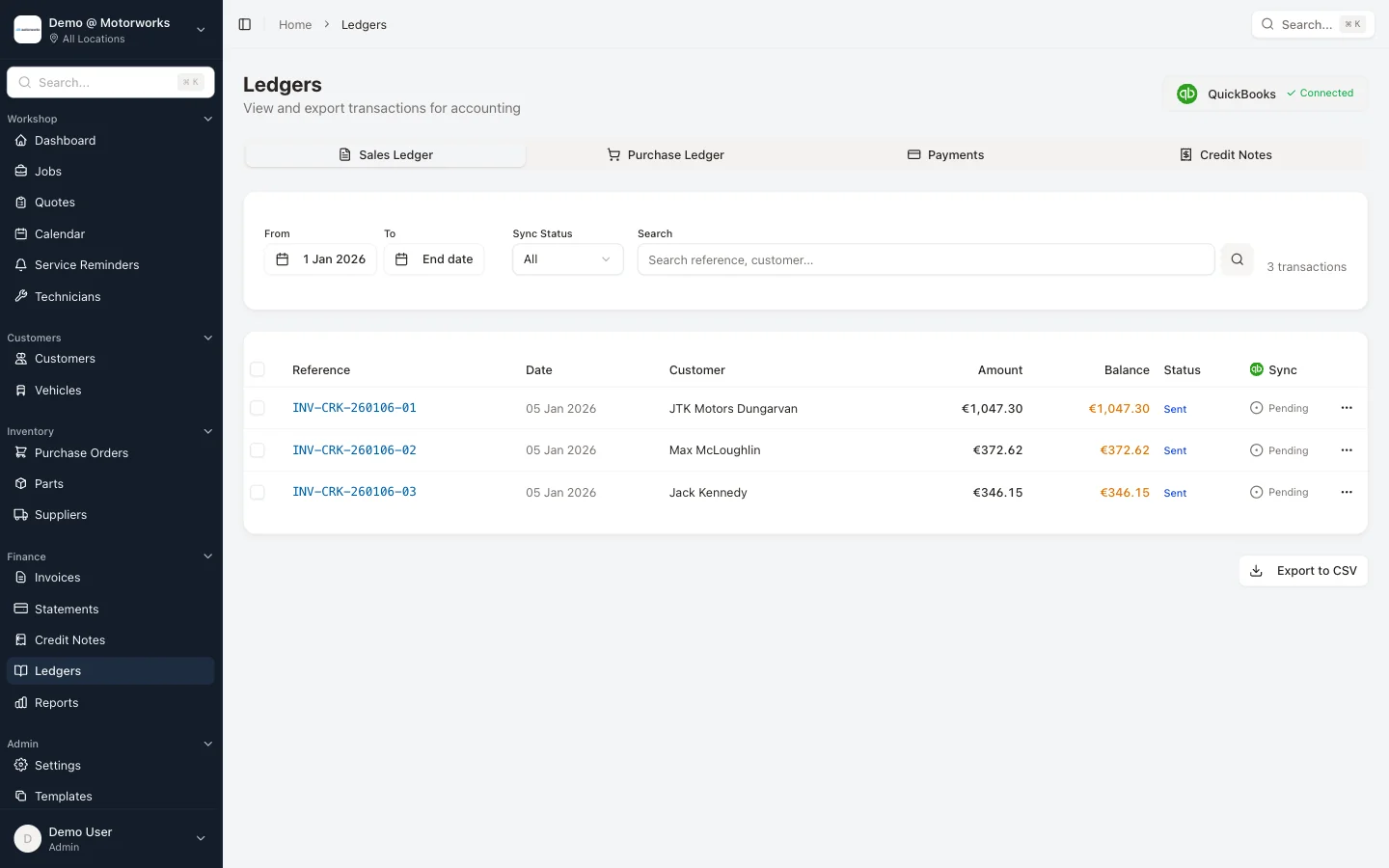

Every invoice is sequential and stored. When an invoice is generated from a job card, it gets the next number in sequence automatically. It’s stored in the system from that point forward, retrievable by date, customer, number, or any other field. If Revenue asks to see all invoices issued between January and June 2024, you can produce that list in minutes. Voided invoices and credit notes are retained with full audit history — nothing disappears from the record.

VAT is calculated correctly at line level. Labour lines apply 13.5%. Parts sold separately apply 23%. The totals flow to your VAT summary, which matches what gets filed on your return. There’s no manual calculation where an error can creep in.

Purchase orders link parts to jobs. Every part ordered is associated with a job, received against a purchase order, and appears on the customer invoice. The audit trail from supplier invoice to customer invoice is complete and traceable — giving you real margin visibility per job, not just an aggregate picture.

Cash and card are recorded together. Sales entered into the system capture the payment method. Cash transactions create the same invoice record as card transactions. Your daily totals reconcile against your lodgement without needing a separate cash book.

Six years of records are maintained automatically. Cloud-based storage means you don’t have to think about archiving. The system keeps everything, accessible from any device whenever you need it — whether that’s next week for an accountant query or in four years for a Revenue check.

Every change is logged. An audit trail records who changed what and when across jobs, invoices, and financial records. If Revenue questions a specific transaction, you can show the complete history of that record — not just the final version.

The invoicing and reporting features in MotorWorks are built around exactly this kind of audit-ready record-keeping. Invoices are generated from job cards, VAT is applied correctly at line level, credit notes maintain a proper paper trail, and every transaction is stored and searchable from the point it’s created.

Common Revenue compliance mistakes Irish garages make

Based on what Revenue identifies in compliance checks and what accountants see in practice when preparing garage accounts, these are the patterns that cause problems most often.

Not issuing invoices for cash sales. The most common and the most serious. Revenue treats uninvoiced cash transactions as undeclared income unless you can demonstrate otherwise. The fix is simple: every transaction gets an invoice, regardless of how it’s paid.

Gaps in invoice sequences. Missing invoice numbers are a red flag. Revenue knows that deleted or voided invoices sometimes represent transactions that have been removed from records. If invoice 1,847 is missing from your sequence, you need to be able to account for it — either as a voided document with a record of the voiding, or explain why it doesn’t exist. A system that issues credit notes rather than deleting invoices avoids this problem entirely.

Mixing personal and business expenses. Claiming personal expenses as business expenses, or running personal transactions through the business account, creates problems for both your VAT claims and your income tax position. Keep accounts completely separate.

Poor cash reconciliation. Lodgements that don’t match cash records, or cash records that don’t exist, make it impossible to demonstrate that cash income was fully declared. Even if everything was correctly declared, the absence of documentation is itself a problem.

Incorrect VAT rates. Applying 23% to labour or 13.5% to standalone parts sales. Both cause your VAT return to be incorrect, and both are detectable.

Inadequate retention. Deleting or discarding records before the six-year period is up. This is typically a process failure rather than deliberate, but it leaves you unable to respond to a Revenue enquiry about an earlier period.

Parts not reconciling to invoices. Significant differences between parts purchased and parts invoiced, with no documented explanation for the gap, raise questions about uninvoiced jobs or stock management.

Preparing for a Revenue check: what to have ready

If you did receive a Revenue notification tomorrow, these are the records you should be able to produce.

- All sales invoices for the period under review, in sequence, with no gaps

- Supplier purchase invoices for the same period, matched to payments

- Bank statements for all business accounts

- Payroll records — payslips, PAYE returns filed through ROS, employment contracts

- VAT returns for the period, with supporting workings

- Cash records — till reports, cash book, lodgement records

- Purchase orders, delivery dockets, and any stock records

The test is not whether the records exist — it’s whether they’re accurate, complete, consistent, and accessible. Records that can be produced promptly and that reconcile with each other put you in a strong position. Records that take weeks to compile and that don’t quite add up do not.

For a broader look at how invoicing record-keeping requirements connect to day-to-day operations, the garage invoicing requirements guide covers the legal obligations on individual invoices in detail.

The practical case for getting this right

Revenue compliance isn’t just about avoiding penalties — though the penalties are real. Incorrect VAT returns can attract surcharges and interest. Failure to maintain adequate records is itself an offence. And a Revenue audit that uncovers significant discrepancies can extend to multiple years, not just the year initially under review.

The more practical case is simpler. Garages with clean, complete records spend far less time and money on accountancy and year-end processing. They’re able to answer Revenue queries quickly and close them out, rather than going through a drawn-out process while trying to reconstruct records from memory. And the same discipline that produces good compliance records also produces the kind of financial visibility that makes a business easier to run — because if you know where every penny in and out is recorded, you know where your money is going.

The garages that handle Revenue compliance easily are not the ones that spend extra time on paperwork. They’re the ones that have a system where compliance is built into the workflow — so doing the work correctly and having the records to prove it are the same thing, not two separate tasks.

If you want to see how MotorWorks handles this in practice — sequential invoicing, credit notes, purchase order tracking, audit logs, and the six-year record archive — book a demo and we can walk you through it. No commitment required.

Frequently asked questions

What records does Revenue require an Irish garage to keep? Revenue requires complete sales records (all invoices, in sequence), purchase invoices for all business expenses, bank records, payroll records, VAT records sufficient to support each return, and cash records if you take cash payments. All records must be retained for six years from the end of the relevant accounting period.

How far back can Revenue audit an Irish garage? Revenue can open a compliance check going back up to six years under normal circumstances. In cases of fraud or neglect, there is no time limit. This is why the six-year retention rule applies — you must be able to produce records for any period within that window.

What triggers a Revenue audit for a garage? Common triggers include high cash turnover relative to declared income, discrepancies between parts purchased and parts invoiced, incorrect VAT rates applied across returns, inconsistent lodgement patterns, or selection as part of a sector-wide compliance campaign targeting the motor trade.

Does a garage need to issue an invoice for every cash sale? Yes. If you are VAT-registered, you are required to issue a VAT invoice for every taxable supply, regardless of how the customer pays. Uninvoiced cash transactions are treated as potential undeclared income in a compliance check.

What happens if invoice numbers are missing in a sequence? Missing invoice numbers are a specific audit trigger. Revenue uses sequential numbering to check whether transactions have been deleted or suppressed. You need to be able to account for any gaps — either as voided documents with a record of the voiding, or explain the sequence break.

How long must an Irish business keep tax records? The minimum retention period is six years from the end of the accounting period to which the records relate. Records relating to 2020 must be kept until at least the end of 2026.

What VAT rates apply to garage work in Ireland? Labour and repair services attract 13.5% VAT. Parts supplied as part of a service or repair also typically attract 13.5% under the composite supply rules. Parts and accessories sold separately attract 23%. Both rates can appear on the same invoice and must be shown separately.